1. How to manage the Company Shares for the Deceased Shareholder, Unfit, Bankruptcy & Merger and Acquisition.

a. When a shareholder deceased and it can be distributed through 3 methods:

Method 1: Grant of Probate (GOP) when the shareholder is having a will.

Method 2: Letters of Administration (LA) when the shareholder is NOT having a will.

Method 3: Distribution Order from Land Administrator if the shareholder is NOT having a will and value of the estate is not more than RM 2 million.

2. What are the steps if the deceased shareholder with A will?

Step 1: All assets will be frozen upon the deceased of the shareholder.

Step 2: Unlock it through a Will by Executor.

Step 3: The executor will execute the will through High Court and get a probate (3-6 months) and unlock the assets.

Step 4: Executor has to ensure all estate taxes and taxes are cleared when delivered to next-of-kin in 18-33 months from the day of the deceased shareholder.

Step 5: The executor will notify to COSEC on the shares transfer with referring to S 109, Companies Act 2016 and the update of shares transfer must be conclude in in longer than 60 days from the day of notification.

Remarks: If the beneficiaries are below the age of 18, the executor will be acting as trustee and dividends receive from company will be distribute to the under-age through trustee.

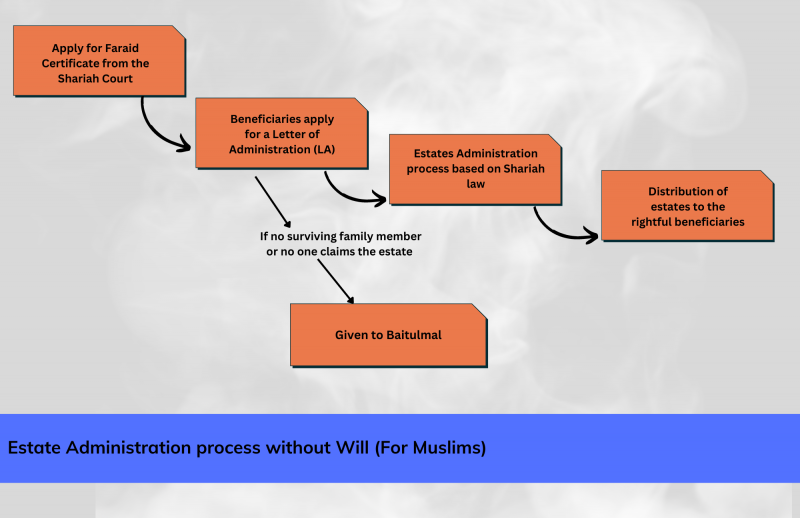

3. What are the steps if the deceased shareholder WITHOUT a will?

Step 1: All assets will be frozen upon the deceased of the shareholder.

Step 2: It can be unlock through identification of heirs (primarily in favor of the spouse (i.e., the legal spouse), issue (i.e., the children and the descendants of deceased children), and parents.)

Step 3: All heirs are to agreed on the estate inclusive of shareholding and announce to the Administrator (the arguments normally begin at this stage due to conflict of interest).

Step 4: Appointment with 2 sureties with Administrator Bond as they will need to guarantee on the entire estate value of the deceased (Distribution Act 1958 ).

Step 5: Application will be made at High Court and upon successful, a Letter of Administration (LA) will be produced.

Step 6: Distribution Order will be distribute according to the list of heirs.

Further reading on the process if without a WILL @ Malaysia: https://says.com/my/lifestyle/what-happens-die-without-will-malaysia

4. Remarks:

a. The scenarios of estate distribution:

a. Scenario 1: If the deceased shareholder is not survive by the immediate heirs, the estate will be distributed according to:

First level: On trust for brothers and sisters of the intestate in equal shares; then,

Second level: For the grandparents of the intestate in equal shares; then,

Thirdly: On trust for uncles and aunts of the intestate in equal shares; then,

Fourthly: For the great grandparents of the intestate in equal shares; then,

Fifthly: on trust for great grand uncles and great grand aunts of the intestate in equal shares.

b. Scenario 2: It is complicated. Just write a Will: https://www.gafsadvisory.com/

5. The scenarios of a shares transfer (Section 105) :

Scenario 1: Deceased of a shareholder

a. Deceased shareholder- estate under administration (S 105 from shareholder to Executor) – Executor/ COSEC doing S 105 to beneficiary.

Scenario 2: Unfit (Mental Health Act 2001) to become a shareholder

a. Unfit shareholder– Court order issued under Committee of Estate ( S 105 from shareholder to Committee of the Estate) – Committee doing S 105 back to Beneficiary’s Name.

Scenario 3: Bankruptcy of a shareholder (Bankruptcy Act 1967 Act 360 – Reprint 2017 )

a. Director General of Insolvency (DGI) takes control of the shares (Section 55 (2) as he is the receiver and reserve the right to S 105 to the same extent Section 55 (3) as the bankrupt shareholder.

Scenario 4: Merger and Acquisition of a member

a. Shareholder under M&A- Restructuring process- Shareholder under M&A doing S 105 to the Successor through a Private Merger Agreement.

6. AmanahRaya also provides Estate Administration services at reasonable rates.

a. Now, you can even access AmanahRaya services digitally via their online portal http://www.amanahraya.my/ where through their hassle-free online services, you can start planning your inheritance today.

b. Other ways to contact AmanahRaya:

Careline: 03-27233 7273

Email: crmd@arb.com.my

Website: www.amanahraya.my

Facebook: AmanahRaya Official

WhatsApp: 03-2055 7557